- (626) 796-6622

- info@firstwilshire.com

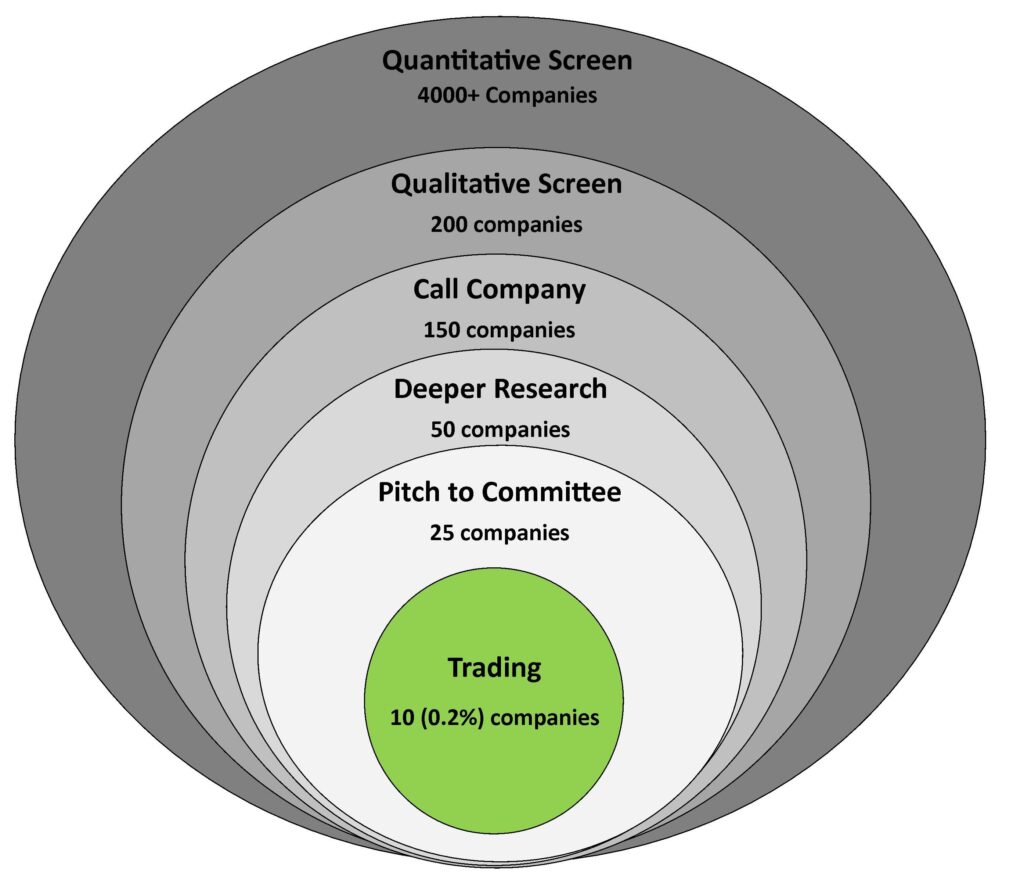

We start by analyzing public information such as financial filings with the Securities and Exchange Commission, press releases, and conference calls with management. In addition to analyzing the numbers, we examine corporate governance and look for signs of accounting red flags. This helps us get up to speed and do our homework prior to interviewing the management. Our proprietary “one-pager” is a great competitive advantage throughout our research process, from initial screens to portfolio reviews.

We firmly believe that interviewing management is an indispensable part of research. These conversations fill in the gaps from simply reading the filings, such as company’s history, culture, and outlook on the future. And we get to know the management. Are they the sort of people we can trust? Are they conservative? Optimistic? Knowledgeable? Boastful? We strive to invest in companies with management that we respect and admire. Following companies for years and regular conversations with the managers allow us to develop a rapport with them and pick up subtle clues about the company’s prospects that would be indiscernible to analysts less familiar with the company.

A model is only as good as the inputs. First Wilshire does not use complex quantitative algorithms. Instead we focus on nailing down the fundamental assumptions. What would be the growth for next year? What about the gross margin? We piece the puzzle together by talking to management, analyzing the company’s prospects, and surveying industry trends. However, there are always risks, uncertainties, and unknowns, so the puzzle is never complete. No model is infallible; instead we allow a margin of safety. In a bad case scenario where the business does not perform as well as reasonably expected, would the company still be undervalued at the current stock price? If yes, then we have our margin of safety.

Corporate frauds and investment scandals demonstrate that investors need to be good detectives when making investments. In our research, we consider the company’s auditor and try to assess whether we can trust the numbers. Where possible, we corroborate the story, as detailed by management and the filings, with other research, such as testing the product, getting a disinterested third party’s opinion, or doing channel checks. We have visited many companies. We are hands-on investors – we like to touch and feel the product, use the service, see the factory. By visiting companies we can gauge their culture, level of activity, sophistication of their operations, and employee morale. Also, it strengthens our relationship with management.

Low valuation relative to assets, earnings potential and cash flow is the primary factor in an investment decision.

We look for companies with long operating histories of revenues and earnings. Turnaround situations are a notable exception. We strive to avoid startups or biotech-type companies that are currently losing money while promising a future payoff. We value a company based on current earnings or near-term projections as opposed to distant future prospects.

Low debt levels relative to assets and equity. Strong balance sheets help companies finance working capital and growth and survive economic shocks.

We look for companies that can grow earnings 15% or more in the intermediate future. These are often companies in emerging industries or growing niches. We would consider a slower-growing company at a very attractive valuation.

If there is little or no analyst coverage, it may be that the company is overlooked by mainstream investors. It may also mean the stock is undervalued. It is easier to find value in an undiscovered company than one widely covered by the analyst community.

Industries with sound economic fundamentals. We prefer companies in industries that are growing. While it is possible to find gems in declining industries, it is usually not wise to swim against the current. Also, stocks in growing industries are more likely to get recognized by other investors, resulting in a quicker return on our investment.

Companies that consistently bring innovative products to market are more likely to maintain their competitive advantage in the future. Such companies tend to exhibit growth and high margins.

Strong, trustworthy management. We interview management to see if they are the type of people we respect and want to work with. We look for management to be knowledgeable, trustworthy and honest as well as capable and energetic. When things are going badly, we want the management to be upfront about it and recognize mistakes, and when business is going well, we want them to recognize the risks and rein in exuberant expectations.

Reported earnings mean little until converted to cash in the bank. We look for companies with strong cash flows after accounting for reinvestment in the business. We do not like industries that require consistent large capital investments. High level of receivables relative to revenues is another warning sign suggesting that the company may need to raise equity or debt in order to fund working capital needs. This is a common pitfall of numerous Chinese companies.

A strong competitive position can be achieved with scale, patented technology, domination of a market niche, or control of a distribution channel. Such companies can grow revenues and margins even in bad times and possibly dominate their industry.

We like management to have a significant stake in the company such that management’s interests are more aligned with shareholders’. However, we are cautious when management owns too much because there is a danger of management running the firm like their private company.

Long-lasting lawsuits drive down the valuation of the stock for an indefinite period of time. Government’s regulatory action is difficult to time or predict. Thus we typically avoid companies that are fighting a lawsuit, benefiting from legal loopholes, or facing impending regulations.

Externalities are costs that are not accounted for in the sale of a product. For example, pollution is an externality of producing certain chemicals. Cigarettes cost a customer, and the public through healthcare costs, more than the price of a pack. We try not to impose moral judgment – our goal is to make money for our clients. But our experience shows that these costs can unexpectedly come back and break the company, sometimes in the form of government regulation or a public backlash, so they must be considered.

Active and honest investor relations efforts, including conference calls with analysts, conference presentations, responsive management and a designated contact for investors. Investor relations efforts increase awareness of and demand for the stock, helping other investors recognize the stock’s value. We avoid companies that are insincere, promotional, and focused on the short term. It is important that they are open in discussing their challenges and opportunities, as well as their strategies to address both.

Stay informed in your investments and the securities Market.

First Wilshire Securities Management, Inc

Copyright © 2021. All rights reserved.