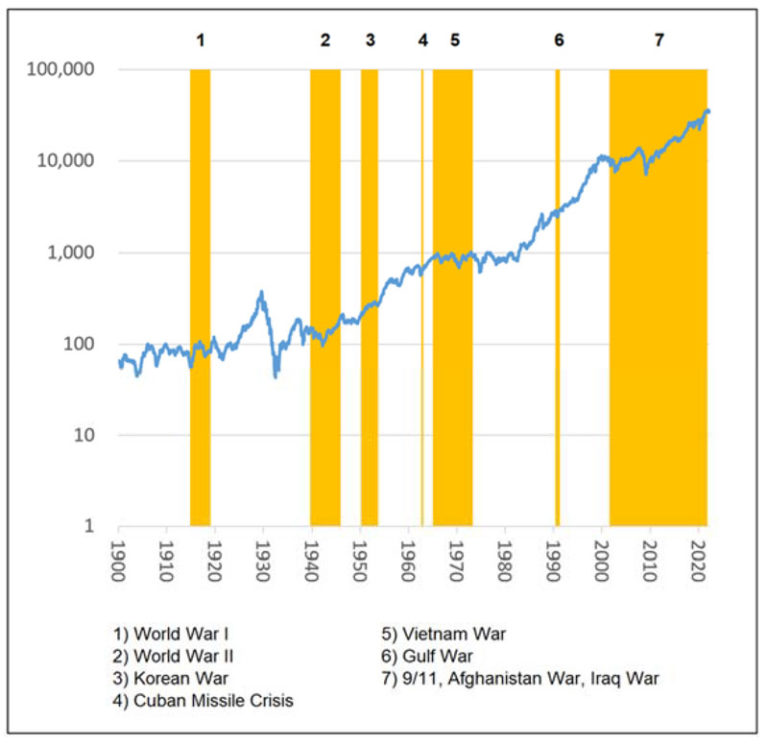

However, if the U.S. should engage in a major conflict, our government will have no choice but to spend even more money on defense. If you think our government has a habit of spending beyond its means and leading us to inflation and currency depreciation, imagine what a major war would do (as a frame of reference: the U.S. debt-to-GDP went from 48% in 1942 to 119% in 1946**, mostly due to World War II). In such a scenario, investors may be well served to stock to investments that could potentially keep up with inflation, rather than being hurt by it. Reasonably strong businesses can keep pace with inflation because they can ultimately raise prices (whereas bonds and cash don’t provide such flexibility). When consumers pay more for products and services, a strong business in the supply chain can get its share.

These are the main reasons why we believe wars, while tragic, have failed to significantly impede the progress of the American economy and stock market. Of course, it doesn’t mean we simply remained static when the Russian invasion occurred. As with any significant event, there will be winners and losers as a result. Some businesses are hurt by the war, while others are immune or could even benefit (for example, defense contractors). We’ve made changes in the portfolio that we believe are warranted. As new developments occur, we will again act as appropriate. It’s important to keep in mind that investment decisions have to be made on a case-by-case basis because each stock has its own unique situation. As we were writing this newsletter, one of our top 10 positions, Antares Pharma, received a buyout offer that sent its stock up almost 50% in a day. It is a company that develops in-home, self-administered drug injection systems and rescue pens. During the Covid-19 pandemic, its business received a strong boost as people stayed home more. But when the pandemic began receding, investors believed these businesses would go away, sending its stock down. However, as we investigated further, we believed many patients would continue to use its technology after seeing the convenience and the reliability it provides. In other words, this is not just a pandemic stock, but a stock whose fortune has been fundamentally changed by the pandemic. How did the war change our investment thesis? We struggled to think of any impact whatsoever. In the end, another pharma company agreed with our assessment and decided to buy the company at a sizable premium. We believe there are always opportunities to be discovered in the small‐cap space, almost regardless of the macroeconomic environment. That’s largely because there are thousands of companies to choose from at any moment, and their stock prices can sometimes fluctuate wildly, presenting us with opportunities. The war has not dampened our enthusiasm to find the next bargain. Not in the least.

Thank you for your continuing trust. We would also like to acknowledge our new clients who recently joined us amidst the market volatility. Welcome aboard.

Sincerely,

First Wilshire Securities Management, Inc.